US to Allow Bitcoin as Mortgage Asset: A Game-Changer or Risky Gamble?

crypto mortgage approval, digital asset valuation in real estate, FHFA cryptocurrency policy 2025

—————–

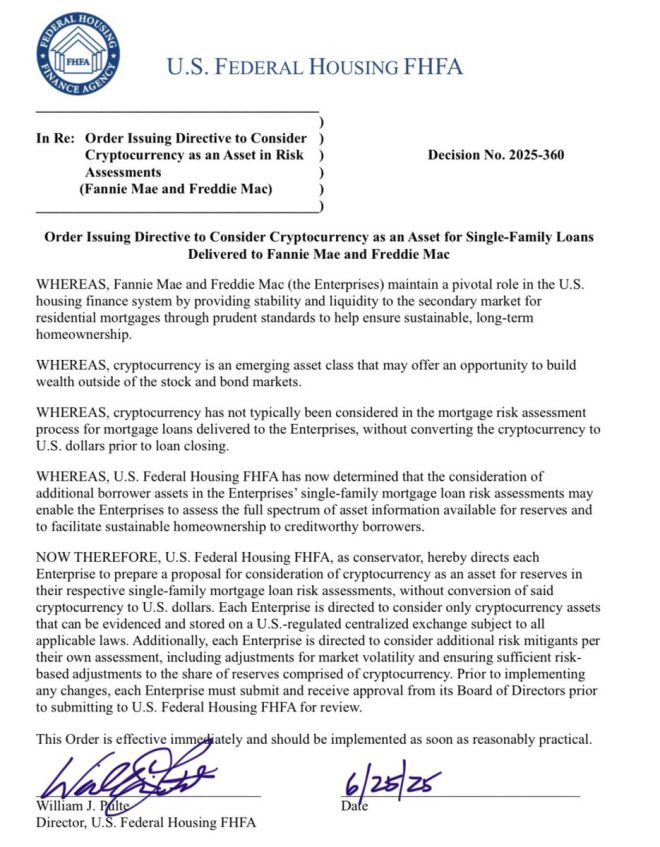

U.S. Federal Housing Finance Agency Allows Cryptocurrency as Mortgage Assets

In a groundbreaking move on June 25, 2025, the U.S. Federal Housing Finance Agency (FHFA) announced a new order that will enable the inclusion of Bitcoin and other cryptocurrencies as valid assets for mortgage applications. This decision marks a significant shift in the traditional view of cryptocurrency within the financial sector and may profoundly impact how individuals secure home loans in the future.

Understanding the FHFA’s Decision

The FHFA, which oversees government-sponsored enterprises (GSEs) such as Fannie Mae and Freddie Mac, issued this order as part of an effort to modernize the mortgage financing landscape. By recognizing cryptocurrencies as legitimate assets, the agency is acknowledging the growing importance and acceptance of digital currencies in the global economy. This decision provides clarity for lenders and borrowers alike, allowing them to utilize their cryptocurrency holdings to secure mortgage loans.

Implications for Homebuyers

The integration of Bitcoin and other cryptocurrencies into the mortgage application process has substantial implications for potential homebuyers:

- YOU MAY ALSO LIKE TO WATCH THIS TRENDING STORY ON YOUTUBE. Waverly Hills Hospital's Horror Story: The Most Haunted Room 502

- Expanded Access to Financing: Many individuals have invested significantly in cryptocurrencies, and this new regulation allows them to leverage those assets to qualify for home loans. This can be particularly beneficial for younger buyers and tech-savvy individuals who may not have traditional assets like savings accounts or stocks.

- Increased Competition: As more individuals enter the housing market with cryptocurrency-backed mortgages, competition among buyers may increase. This could lead to a more dynamic real estate market, with sellers potentially receiving higher offers.

- Financial Literacy and Education: With the rise of cryptocurrencies in mainstream finance, there is a growing need for education on how these assets can be effectively used in the mortgage process. Lenders may need to provide additional resources to help borrowers understand the implications of using digital currencies in their applications.

Challenges and Considerations

While the FHFA’s decision is a significant step forward, it is not without its challenges:

- Volatility of Cryptocurrencies: One of the primary concerns surrounding the use of cryptocurrencies as assets is their notorious price volatility. Lenders will need to develop strategies to assess the value of these assets adequately and mitigate risks associated with sudden market fluctuations.

- Regulatory Framework: The incorporation of cryptocurrencies into the mortgage lending process raises questions about regulatory compliance and consumer protection. There may be a need for new guidelines that specifically address how cryptocurrencies can be used in this context, ensuring that both lenders and borrowers are protected.

- Valuation and Appraisal: Determining the value of cryptocurrency assets for mortgage purposes can be complex. Unlike traditional assets, cryptocurrencies can experience rapid price changes. Lenders will need to establish clear methodologies for valuing these assets to ensure fair loan amounts.

The Future of Cryptocurrency in Real Estate

The FHFA’s order is likely to pave the way for further integration of cryptocurrencies in various sectors of finance, including real estate. As more institutions adapt to the digital currency landscape, we can expect to see several trends emerging:

- Increased Adoption by Financial Institutions: With the recognition of cryptocurrencies as assets, more banks and financial institutions may begin to offer services tailored to crypto investors. This could include specialized mortgage products or financial advice for utilizing digital currencies in real estate transactions.

- Emergence of Crypto-Real Estate Platforms: The real estate industry may see the rise of platforms specifically designed to facilitate transactions using cryptocurrencies. These platforms could streamline the buying and selling process, making it easier for crypto investors to enter the real estate market.

- Innovation in Mortgage Products: As the market evolves, we may see innovative mortgage products that cater to cryptocurrency holders. This could include options with flexible terms based on the performance of the asset or loans that adjust in line with cryptocurrency market trends.

- Global Influence: The U.S. decision could inspire other countries to consider similar regulations, leading to a more unified approach to cryptocurrency in the global real estate market. This could facilitate international transactions, allowing investors from around the world to leverage their digital assets in different markets.

Conclusion

The FHFA’s order to allow Bitcoin and cryptocurrency to be counted as assets for mortgages represents a pivotal moment in the intersection of digital finance and real estate. As the landscape evolves, both lenders and borrowers will need to adapt to the new realities of cryptocurrency in mortgage lending. Education, regulation, and innovation will be crucial in navigating this new frontier, and the potential benefits for homebuyers are significant.

As the integration of cryptocurrencies into the mortgage process continues to unfold, it is essential for all stakeholders—buyers, lenders, and regulators—to stay informed and engaged. The future of real estate financing is undoubtedly changing, and embracing these changes could lead to a more inclusive and dynamic housing market.

JUST IN: US Federal Housing Finance Agency issues order to count Bitcoin & crypto as an asset for a mortgage. pic.twitter.com/tzRZeJb1tq

— Bitcoin Magazine (@BitcoinMagazine) June 25, 2025

JUST IN: US Federal Housing Finance Agency Issues Order to Count Bitcoin & Crypto as an Asset for a Mortgage

Big news just dropped! The US Federal Housing Finance Agency (FHFA) has decided that Bitcoin and other cryptocurrencies can now be counted as assets when applying for a mortgage. This is monumental, especially for those looking to buy homes in today’s digital economy. Let’s dive into what this means for potential homebuyers, the real estate market, and the broader implications for cryptocurrency.

Understanding the Implications of the FHFA’s Decision

First things first, this decision opens a lot of doors for people who hold cryptocurrencies. Traditionally, mortgage lenders have been hesitant to recognize anything other than cash, real estate, or income as assets. But now, if you’ve got a stash of Bitcoin or other digital currencies, you can leverage that value when applying for your mortgage. This could significantly change your buying power and help you secure a home loan that was previously out of reach.

Imagine walking into a lender’s office and saying, “I want to use my Bitcoin to buy a house.” That’s a game-changer! It could also attract a younger demographic who are more engaged with digital currencies and are looking to invest in real estate.

What Does This Mean for Homebuyers?

For homebuyers, this opens up a new pathway to homeownership. If you’ve been investing in Bitcoin or holding onto other cryptocurrencies, you now have the opportunity to utilize those assets for one of the biggest purchases of your life. This could make a huge difference, especially in a market where traditional assets like cash savings may not be sufficient to cover rising home prices.

Additionally, this could encourage more individuals to invest in cryptocurrencies, knowing that they can use those assets to facilitate significant purchases. It’s a win-win situation, as it could potentially increase the number of people entering the housing market.

How Will Lenders Respond?

Of course, the next big question is how lenders will respond to this change. It’s one thing for the FHFA to make this ruling; it’s another for banks and mortgage companies to adopt it. Lenders are typically cautious, and they will likely want to establish guidelines on how to assess the value of cryptocurrencies. They may set up specific criteria to evaluate the volatility and liquidity of these digital assets.

It’s also possible that lenders will need to develop new technologies to verify cryptocurrency ownership and value easily. This may lead to partnerships with fintech companies specializing in digital assets, further integrating cryptocurrency into the traditional financial landscape.

The Bigger Picture: A Shift in the Housing Market

The FHFA’s decision could signify a significant shift in the housing market. With more people potentially entering the market, we might see increased competition for homes. This could drive prices up even more, especially in already hot markets. However, it could also lead to a more diverse pool of buyers, which might stabilize prices in the long run.

Furthermore, as cryptocurrencies continue to gain acceptance in various sectors, we may witness increased interest from real estate developers and investors. They could start accepting Bitcoin and other digital currencies as payment for properties, further blurring the lines between traditional finance and the evolving world of digital assets.

Challenges Ahead: Volatility and Regulation

While this development is exciting, it’s essential to consider the challenges that come with it. The volatility of cryptocurrencies can pose a risk for both lenders and borrowers. Imagine applying for a mortgage with a Bitcoin asset that suddenly drops in value. Lenders will need to find ways to mitigate these risks, possibly through stricter lending criteria or higher down payment requirements.

Regulatory considerations will also play a significant role in how this decision unfolds. As cryptocurrencies continue to evolve, governments and regulatory bodies will need to establish clear guidelines to protect both consumers and financial institutions. This might include ensuring that lenders conduct thorough assessments of a borrower’s cryptocurrency holdings and understanding the potential risks involved.

What This Means for the Future of Finance

The recognition of Bitcoin and crypto as assets for mortgages could be the beginning of a broader acceptance of digital currencies in the financial system. As more institutions recognize the value of cryptocurrencies, we might see a shift towards a more integrated financial ecosystem where traditional and digital assets coexist.

This decision also highlights the growing need for financial education around digital assets. As more people enter the housing market using cryptocurrencies, it’s crucial for them to understand how these assets work, their risks, and how to manage them effectively. Educational programs and resources will become increasingly important to ensure that buyers are well-informed.

Final Thoughts: Embrace the Change

The US Federal Housing Finance Agency’s move to allow Bitcoin and crypto as assets for mortgages is a significant step forward in the integration of digital currencies into mainstream finance. It opens up new possibilities for homebuyers and could lead to a transformation in how we view and utilize cryptocurrencies in the real estate market.

As we navigate this new landscape, it’s vital to stay informed and adapt to the changes. Whether you’re a seasoned cryptocurrency investor or just dipping your toes into the waters, understanding the implications of this decision will be key to making the most of the opportunities ahead.

Stay tuned as we continue to monitor how this situation develops and what it means for the future of home buying and finance. The landscape is changing, and it’s an exciting time to be involved in both the housing and cryptocurrency markets.